May 26, 2025

Looking to put your crypto assets to work or explore alternatives to conventional lending? Crypto lending might be the solution you’re looking for. This innovative model is rapidly gaining traction among investors and borrowers, offering decentralized platforms where users can lend or borrow digital assets like Ethereum or Bitcoin. As of May 2, 2025, lending protocols held approximately $45.261 billion in total value locked (TVL), according to DeFiLlama, though this number fluctuates with market conditions. But with rapid growth comes essential questions: Is crypto lending safe for long-term investors and everyday users?

In this guide, we’ll explain how crypto lending works, outline its key benefits and risks, and spotlight top platforms dominating the space, helping you make strategic decisions about participating in this growing DeFi ecosystem.

What Is Crypto Lending?

Crypto lending is a growing service in decentralized finance (DeFi). It allows users to lend their digital assets to earn interest. Much like a traditional savings account, lenders receive periodic returns on their deposited cryptocurrencies.

Crypto lending platforms may be decentralized or centralized, and interest rates can vary based on platform policies and market demand.

On the other hand, Borrowers can access loans by using their crypto as collateral, helping them retain long-term holdings. However, they risk liquidation if asset prices drop sharply. This is especially useful when selling may result in a loss during bear markets.

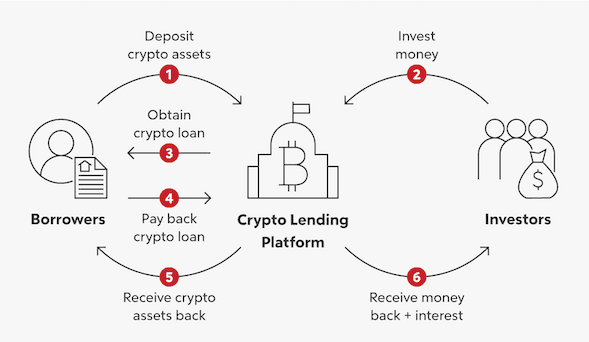

How Does Crypto Lending Work?

Getting started with crypto lending involves selecting a secure and reputable platform. Popular platforms include Aave, Compound, Morpho, and Nexo. Always research current reputations and regulatory status before using any lending service. The process usually looks like this:

Step 1: Create an Account

Initiate the process by signing up with your chosen crypto lending provider. It often involves identity verification (KYC), email registration, and setting up account credentials.

Step 2: Deposit Crypto

Once verified, transfer the cryptocurrency you intend to lend or use as collateral into your platform wallet.

Step 3: Select Lending or Borrowing

Decide if you’d like to lend your crypto and earn some passive income, or if you’d prefer to borrow funds by putting up your crypto as collateral. If you’re leaning towards lending, you can choose which asset you want to lend, the interest rate you’re comfortable with, and how long you want to lend it. If borrowing sounds better, you can decide how much you want to borrow, the terms that work for you, and which crypto you’ll pledge as security. Interest rates are generally algorithmically determined by supply and demand, and lenders do not manually select interest rates or lending durations.

Step 4: Platform Approval

Some platforms may use smart contracts and require overcollateralization for decentralized approvals before finalizing the transaction.

Step 5: Receive or Disburse Funds

If lending, your crypto will be matched with a borrower. If borrowing, you’ll receive funds (often in stablecoins or fiat) once your collateral is locked in.

Step 6: Payments and Earnings

Borrowers must repay the loan with interest over the agreed term. Lenders receive interest payouts, often monthly or as agreed per contract.

Step 7: Close the Loan

At the end of the loan period, borrowers repay the principal and any remaining interest to unlock their collateral. Lenders receive their crypto back along with accrued interest.

Let’s understand the process by an example: You choose to lend 2 Bitcoin through a crypto lending platform for 90 days at an interest rate of 6%. These funds are allocated to lending pools or smart contracts where institutional borrowers, subject to platform-specific terms and risk, may access them. An institutional borrower uses your BTC as a loan, backed by collateral, to pursue short-term market opportunities. After 90 days, they repay the original 2 BTC plus 6% interest, allowing you to earn passive income without selling your Bitcoin. However, in most DeFi lending, funds go to a shared lending pool. Borrowers draw from the pool; lenders collectively earn interest from the pool’s borrowers.

After grasping the basics of how crypto lending works. Let us see the different types of lending platforms.

Also Read: Making Money in a Crypto Bear Market: Strategies and Ways

Types of Crypto Lending Platforms

Crypto-backed loans are typically offered through two broad categories: centralized platforms (CeFi) and decentralized protocols (DeFi), though hybrid models also exist. Here’s how they differ:

Centralized Finance (CeFi):

CeFi lending is facilitated by centralized platforms operated by companies that manage the lending process. Investors lend or borrow crypto through these services, but the company retains custody of the assets during the loan term. While CeFi offers user-friendly services, it’s prone to custodial and transparency risks, as shown by the bankruptcies of Celsius, BlockFi, and Voyager in 2022.

Decentralized Finance (DeFi):

DeFi lending uses blockchain-based peer-to-peer protocols. Unlike CeFi, DeFi platforms allow users to manage assets via smart contracts, but custody may vary based on protocol design and wallet configuration. This trustless model offers more transparency but may require more technical knowledge. Strictly speaking, in DeFi lending, users retain custody of their private keys (non-custodial) and interact with smart contracts. However, the actual “control” of funds while locked in lending protocols depends on smart contract permissions — users can’t arbitrarily move lent funds until the loan term ends or is repaid. This is a subtle nuance between self-custody of keys and custody of locked assets.

Now that you understand the two primary types of crypto lending platforms, CeFi and DeFi, it’s time to explore how to benefit from them. Whether you choose a centralized provider or a decentralized protocol, both offer opportunities to earn interest on your digital assets. Let’s break down how you can turn your crypto into a reliable source of passive income.

How to Earn Passive Income Through Crypto Lending?

Crypto lending offers a smart way to generate passive income from digital assets. Here’s how you can make the most of it:

Pick a trusted platform: Choose a well-established crypto lending platform with strong security, positive reviews, and clear terms. Your platform choice is key to protecting your assets.

Define your strategy before you start lending: Decide how much crypto you want to lend and for how long. Longer durations may yield better returns, but they also come with added risk. Having a clear strategy will help you stay in control of your lending activities.

Set a fair interest rate: Aim for a competitive yet reasonable rate. Higher rates may be tempting, but they could increase the chances of borrower defaults.

Smart risk management: It is essential for successful crypto lending. In case of DeFi, diversifying your lending portfolio and continuously monitoring collateral ratios and protocol-level risk metrics, rather than individual borrower profiles, can help safeguard your assets.

Reinvest earnings: Consider reinvesting the interest you earn to gradually boost your returns over time.

Also Read: Earning Passive Income with DeFi Lending and Interest

Cryptocurrency lending can become a steady income stream by planning wisely and staying cautious without selling your assets. Now let’s look at the Top lending platforms 2025 based on TVL as of 02.05.2025.

Top 5 DeFi Lending Platforms (May 2025)

With DeFi continuing to reshape global finance, crypto lending platforms are leading the charge, offering users a way to earn yield or access capital without intermediaries. Below are the top 5 DeFi lending platforms dominating the space as of 02.05.2025.

1. Aave V3

TVL: $20.31 billion

Chains Supported: Ethereum, Arbitrum, Avalanche, Optimism, Polygon, Base, Scroll.

Key Features:

Flash loans.

Multi-chain liquidity pools.

Staking via the AAVE token.

Recent Developments: Aave V3 has expanded to Layer-2 networks like Base and Scroll, enhancing scalability and reducing transaction costs.

2. JustLend

TVL: $3.75 billion

Platform: Built on the Tron blockchain.

Key Features:

Users can pay fees in USDT instead of TRX, and 90% of gas costs are subsidized, making lending more accessible.

Interest adjusts with market supply-demand shifts.

Recent Developments: In February 2025, Justin Sun discussed USDD’s growth potential and its relationship with JST, emphasizing the strategic importance of these tokens within the TRON ecosystem.

3. Morpho

TVL: $2.876 billion

Platform: Built on the Ethereum blockchain

Key Features:

Morpho allows users to tailor their risk-reward profile by selecting from curated vaults, markets, or products.

It provides higher collateralization factors with its isolated lending markets, improved interest rates, and low gas consumption.

Recent Developments: Morpho is advancing its Morpho Blue architecture, a modular lending layer that enables developers to create custom, isolated lending markets.

4. Compound Finance

TVL: $2.352 billion

Platform: Built on the Ethereum (ETH)

Key Features:

Utilizes dynamic rates based on supply and demand, enabling efficient money market operations.

Users receive interest-bearing cTokens when lending assets, allowing for composability across DeFi.

Recent Developments: Compound has recently launched Compound III (Comet), a streamlined version focused on reducing risk by isolating collateral assets per market.

5. SparkLend

TVL: $2.222 billion

Platform: Built on the Ethereum blockchain.

Key Features:

It offers decentralized lending and borrowing services.

Focuses on providing stable and secure lending options.

Recent Developments: SparkLend has gained traction due to its focus on capital efficiency and integration with the MakerDAO ecosystem. It offers users exposure to DAI-backed lending products.

Also Read: Safest Ways to Store Cryptocurrency in 2025

Benefits and Risks of Crypto Lending

Crypto lending has surged in popularity as a way for users to earn passive income or access quick liquidity without selling their assets. While the returns can be attractive, weighing the potential risks before participating is essential.

Below is a table summarizing the key benefits and risks of crypto lending to help you make informed decisions:

Benefits | Risks |

High Returns: Some crypto lending platforms offer APYs between 4% and 10%, although these rates fluctuate with market demand and carry corresponding risk. | Crypto Volatility: Price swings can reduce the value of collateral or the lent assets. |

Portfolio Diversification: Enables investors to diversify into income-generating crypto assets. | Counterparty Default: Borrowers may fail to repay, resulting in potential asset loss. |

Flexible Terms: Offers short-term lending, early withdrawals, and customizable loan durations. | Platform Security Vulnerabilities: Hacking incidents or smart contract bugs can lead to permanent fund losses. |

For those who want to earn passive income from crypto without the risks of lending, such as borrower defaults or market volatility, alternative DeFi solutions like stablecoin yield protocols may offer a safer path. One such option is Sperax, which allows users to earn yield on its native stablecoin yield aggregator USDs through automated on-chain mechanisms without engaging in lending.

Also Read: Benefits and Working of Staking Crypto in Cold Wallets

Earning Passive Income with Sperax: A Safer Alternative to Conventional Crypto Lending

If you’re looking for a more stable way to earn yield in crypto, Sperax offers an innovative approach. Instead, Sperax operates a fully decentralized stablecoin yield aggregator protocol that allows users to earn passive income simply by holding USDs. Moreover, its yield optimizer also helps you earn passive income easily.

How Sperax Yield Works

Sperax combines the benefits of decentralized finance (DeFi) with stability:

Auto-Yield with USDs: When you mint or USDs and hold them in your wallet, it automatically yields no need to stake or lend manually.

Risk-Minimized Returns: Yield is generated through decentralized reserve management, which reduces exposure to default risks.

Fully On-Chain and Transparent: Sperax operates transparently with audited smart contracts you can verify, unlike some lending platforms that rely on centralized management.

Why Choose Sperax Over Conventional Lending?

Sperax (USDs) | Crypto Lending Platforms |

Auto-yield with flexible access, though liquidity may vary during high market activity. | Requires active participation or lock-up periods. |

No counterparty risk. | Exposed to borrower defaults. |

Can mint or redeem 1:1 for USDC, USDT or USDC.e. | Yield depends on the volatility of lent tokens. |

Fully on-chain, DeFi-native. | It is a mix of centralized and decentralized platforms. |

Whether you’re risk-averse or simply looking to diversify away from high-volatility strategies, Sperax offers a compelling solution to earn yield passively with fewer trade-offs than those that come with crypto lending.

Conclusion

Whether you want to make some money on the side with your crypto or need cash without selling it, crypto lending can be a great option. But like any money move, it’s super important to think about how much you could earn versus how much you could lose due to things like market ups and downs, borrowers not paying back, or even issues with the lending platform.

To keep your money safe, figure out how much risk you’re comfortable with, shop around for the best lending platform, and keep up with the latest in the DeFi world. And if you want a less risky way to make money than conventional lending, check out Sperax. They let you earn interest on stablecoins, which are tied to the US dollar, without having to lend anything out.

Start earning passive yield with Sperax today at www.sperax.io

FAQ

Q. Is crypto lending safe for beginners?

Crypto lending can be safe for beginners if they use well-audited platforms and understand the risks, such as smart contract bugs, volatility, and counterparty failure.

Q. What are the main risks in crypto lending?

Key risks include platform hacks, smart contract bugs, collateral liquidation due to volatility, and the absence of regulatory protection for lenders or borrowers.

Q. Can I lose money through crypto lending?

Yes, you can lose funds due to price crashes, platform insolvency, or unexpected liquidations. Continually evaluate risk before committing assets.

Q. How do lending platforms ensure crypto lending safety?

Top platforms use over-collateralization, audits, insurance, and liquidation protocols to reduce risk and enhance user trust. However, not all platforms insure user funds, and insurance is often partial or protocol-specific.

Q. Is decentralized or centralized crypto lending safer?

Centralized platforms offer more customer support but carry custodial risk. Decentralized platforms reduce third-party risk but depend on smart contract security.

Q. What’s the safest way to start crypto lending?

Start with a small amount on a reputable, audited platform. Use stablecoins to minimize volatility and monitor collateral ratios closely. Beginners are suggested to use platforms with transparent track records (e.g., public audits, time in operation, open-source contracts for DeFi).